The Allure (and Reality) of Private Investments

It’s not unusual to feel a twinge of FOMO when everyone seems to be talking about the next big investment trend. Lately, private equity, private credit, and other “alternative” investments have been stealing the spotlight.

What used to require millions to access is now open to individual investors with smaller commitments. The pitch sounds great: access to the kinds of deals once reserved for big institutions or ultra-wealthy families, along with the promise of higher returns and diversification.

But, as with most things in investing, the story is more complicated than the sales pitch.

The Upside Investors Hear

- Diversification: Private investments don’t move in sync with public stocks and bonds, which can make portfolios look more stable.

- Return Potential: Some private funds have posted strong results and outperformed traditional markets.

- New Opportunities: You can gain exposure to businesses and strategies not available in the public markets.

The Fine Print Investors Often Miss

- Manager Risk: Performance varies widely. Results depend heavily on the skill of the fund manager. Top-performing funds can shine, but plenty fall short. Large institutions have entire teams devoted to spotting the difference, yet results still vary dramatically.

- Liquidity Limits: Unlike stocks and bond funds, private investments often tie up your money for years. Even “interval funds” that allow occasional withdrawals can freeze redemptions if too many people want out at once.

- Valuation Smoothing: Private investments may look steadier simply because they’re priced infrequently, not because they’re immune to market downturns.

- Costs & Complexity: Fees tend to be higher, and the paperwork can be a hassle—K-1 forms, extensions, and limited transparency can eat into returns.

- Concentration & Overlap: Many private funds own only a handful of companies. And if you already have exposure through your career or business, you might be doubling up on the same kinds of risks.

- Buyer Beware: If the domain of large institutions and highly experienced investors is opening to a wider audience, investors need to be even more careful and informed. Will enough investors do the work to be?

The Irony of It All

Plain-vanilla public markets have delivered excellent returns in recent years, yet many investors are looking elsewhere for something “better.”

We’ve seen this movie before. In the early 2020s, SPACs and thematic ETFs tied to trends like clean energy, blockchain, and space exploration exploded in popularity. By 2023, many of those “can’t-miss” investments had fallen hard, some by more than 75%, while plain old U.S. stocks quietly kept compounding at double-digit rates.

Here’s a comforting fact: buying at market highs has historically worked out just fine for patient investors. New highs aren’t warning signs; they’re signs of strength.

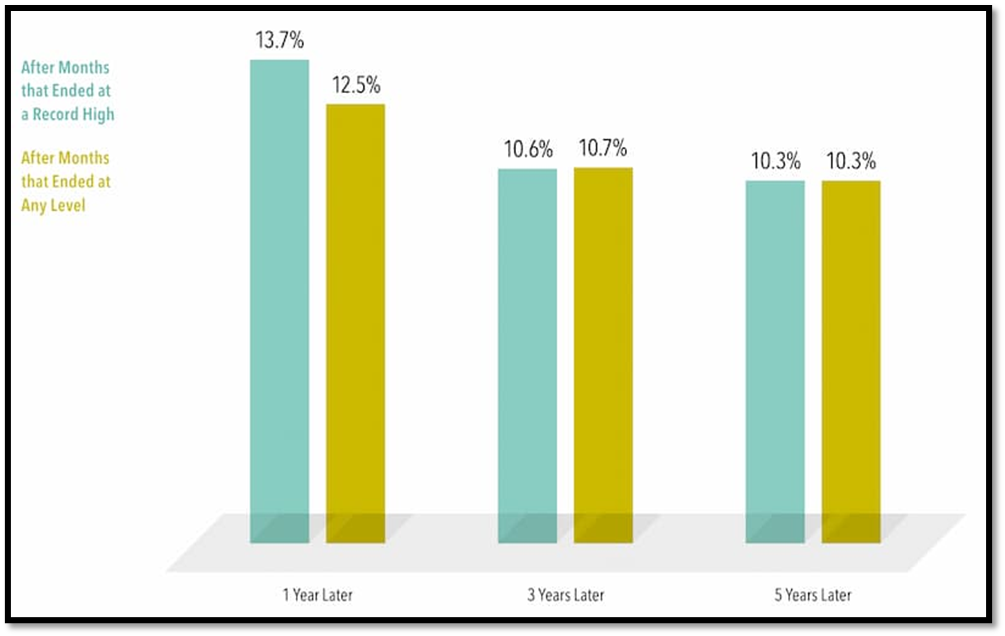

U.S. Stock Market, S&P 500 INDEX, AVERAGE ANNUALIZED COMPOUND RETURNS 1926–2024

Past performance is no guarantee of future results. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio. In USD. For illustrative purposes only. New market highs are defined as months ending with the market above all previous levels for the sample period. Annualized compound returns are computed for the relevant time periods subsequent to new market highs and averaged across all new market highs observations. There were 1,187 observation months in the sample. January 1926–December 1989: S&P 500 Index, Stocks, Bonds, Bills and Inflation Yearbook™, Ibbotson Associates, Chicago. January 1990–present: S&P 500 Index (total return), S&P data © 2025 S&P Dow Jones Indices LLC, a division of S&P Global. All rights reserved. Provided by Dimensional Fund Advisors LP, an investment advisor registered with the Securities and Exchange Commission.

As the chart above shows, 31% of all monthly closing levels were new highs over the last 98 years between 1926 and 2024 for the U.S. stock market, S&P 500 Index.

After those highs, the annualized returns ranged from almost 14% one year later to more than 10% over the next five years, which were close to average returns over any period of the same length.

While a market correction will come sooner or later, history shows that staying the course tends to be the winning strategy.

Chasing alternatives can mean overlooking what’s already working.

The Bottom Line

Private markets aren’t good or bad, they're just different. For certain investors with significant resources, long time horizons, and a tolerance for costs and complexity, they may play a role. But for most, the transparent, liquid, and diversified public markets remain the most reliable way forward.

The smarter question isn’t:

“Are private assets good?” but “Do they really fit my goals, liquidity needs, and capacity to evaluate them?”

Because sometimes, the smartest move isn’t chasing what’s new, it’s sticking with what’s proven.

At Open Window, we help families answer those questions with clarity and confidence. Reach out to (775) 827-0670 or schedule a 'Quick Connection' time with Eric, Joe, or Brendan at www.openwindow.com/connection.